I think it's much more a matter of negative real interest rates. This inflates the price of all assets, but especially real estate, which is available to be purchased with the cheapest fixed-rate leverage around.

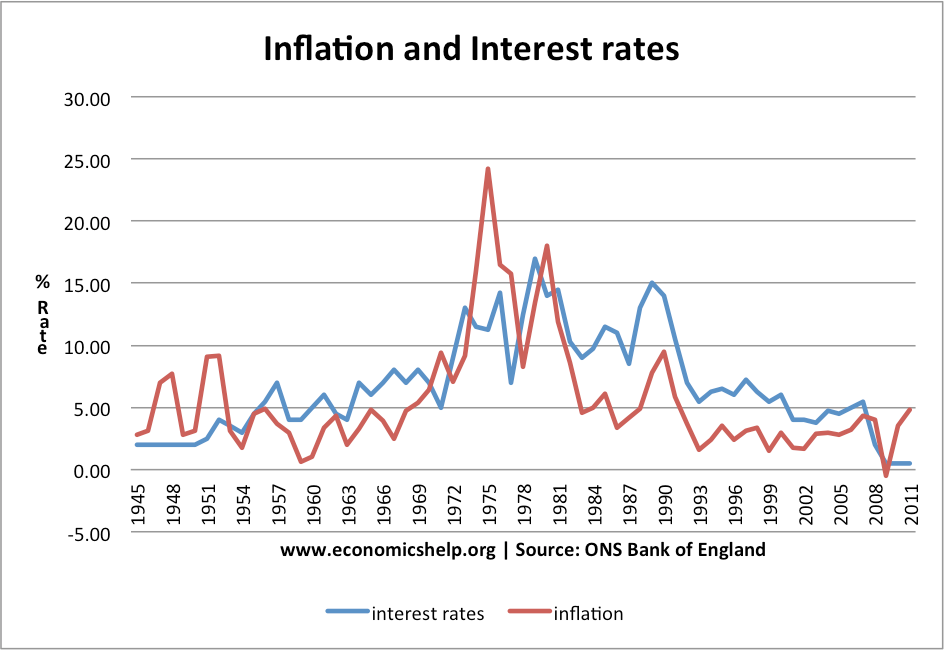

Ah, yes-- I forgot to mention that. I was astounded when my father mentioned recently that when they bought the home I grew up in, the interest rate was 12%!

Right now, living in a suburb with people from the nearby city fleeing for greener pastures in my area or further out still, the paper value of my home is up 10% in a year-- as you say, making any loan on nearby homes effectively a negative rate.

Whereas using the interest rates my parents paid, a mortgage

today for the same amount as they had, at their interest rates, would have 3x the monthly payment. The house itself is about 3.5x the original price, making the gap between effective living costs much smaller than the nominal sticker price on the house would make it seem.

The "don't buy a home mortgage for more than 2x-3x you annual salary" was advice formed at a time of much higher interest rates.

> I was astounded when my father mentioned recently that when they bought the home I grew up in, the interest rate was 12%!

The prices of houses adjust very quickly to changes in interest rates because housing prices are based on what an "affordable" mortgage payment for the market is. Housing prices change to make that math work.

Interest rates and housing prices only matter to people who are buying a house that aren't selling one at the same time. Low interest rates are bad for first time home buyers and investors.

> The "don't buy a home mortgage for more than 2x-3x you annual salary" was advice formed at a time of much higher interest rates.

Also, when that adage was coined, the cost of the "essentials" required to live hasn't gone up as much so people have more of their income to spend on housing.

True: people can afford $X/month. The proportion that goes towards interest is less relevant.

In fact, I'd prefer a lower sticker price & higher interest rate to get to $X. That way when interest rates inevitably drop at some point I can refi at the lower rate and get the partial benefits of both lower sticker $ and interest %.

It's funny. The reason you hear all those stories about boomers being able to afford a house, college education etc on a basic salary is primarily due to the higher interest rates of the time.

Buying a house when rates were 10% and watching them drop to next to 0 over 30 years must've been fun.

Of course Re: college there are other reasons, like government derisking lending by backing the loans, supporting higher and higher costs.

But it should be no surprise that debt fueled expenses are much much higher now. You can certainly say that carrying costs may be similar due to lower rates, but personally I'd much rather buy an asset at a high rate, and have the option of paying down quickly to become debt free.

Nowadays it's almost nonsensical to pay down your debt from an opportunity cost perspective. But even if carrying cost is low, there's an uncomfortable feeling when you live life by financing everything, and with high level of debt.

The question is, will we ever normalize, or will we follow Europe to negative rates?

The current Fed is too politicized to normalize policy. I think partly due to the greater public scrutiny of their moves. Almost everybody will vote for easy money if you give them the choice. Easy money is always the right choice in the very short term. The longer term distortions are the thing to worry about.

Lowering rates effectively initiates a one time transfer of wealth from the future generations to the present.

Central banks can only set the nominal rate of interest. The real rate of return on capital is independent from monetary policy. If the central bank sets the nominal rates below the real rate, it's possible to make a profit by borrowing money at the nominal rate and investing it in a business and earning the real rate.

Yes, but the central bank influences the real rates. Real rates are a function of the nominal rates and level of inflation.

Tighter monetary policy will lead to lower levels of inflation, thus higher real rates.

Central banks are also doing QE and distorting nominal rates on treasuries by shrinking their supply in the market. e.g. Fed buys a 10yr treasury, now it sits on their balance sheet for the next 10 years, rather than floating in the free market.

If the Fed hadn't bought trillions of treasuries over the last two years, what would the nominal yield on treasuries be?

Beyond the mechanical, the Fed has created a psychology that the treasury market is no longer a free market, which discourages investors to sell or go short.

Similar to equities. People believe the Fed will backstop any turmoil, so valuations begin to matter less.

So current Fed policy pushes both variables in the equation towards lower real rates, both in mechanical and in psychological terms.

> Tighter monetary policy will lead to lower levels of inflation, thus higher real rates.

Tighter monetary policy will also lead to higher nominal rates. Nominal rates, inflation and the quantity of money cannot be set independently of one another.

You seem to be in agreement with me then. Higher nominal rates will also lead to lower inflation, thus pushing real rates even higher. So a hike acts on both the inflation side and nominal rate side to push real rates higher.

But speaking to the immediate circumstances, the fed primarily influences the short end of the rate curve. (Once QE is ended)

If the fed were to surprise hike interest rates this week, you can bet yields on the long end of the curve would come down.

Because the market would anticipate a hike in short term rates leading to end of inflation fears, and potentially triggering a deflationary event due to the surprise nature of it.

E.g. recall the times when the yield curve becomes inverted.

You can see over the past two weeks the yield curve has started inching towards an inversion. Actually the 20yr and 30yr inverted for the first time ever last week.

It's only speculation to say what this means, but to me seems a pretty obvious signal that the market expects the Fed to have to tighten faster than they're saying to curb inflation.

E.g. look at how quickly the 2yr has risen, while the 10yr has been in decline

Of course this inversion move is almost entirely due to how slow the Fed has moved. If they had moved faster, there would be less concern with a tightening. Now they may be late to the game if inflation pressures don't begin to ease soon.

We may actually be at full employment already, due to lifestyle changes leading to permanently lower labor force participation rate. In which case the Fed is years behind the curve on tightening. We'll know after a few more employment reports.

No, we are in disagreement. I agree with the view that the real rate is determined by the supply of savings and the demand for funds. According to this view, in the context of monetary policy, the real rate of interest is an exogenous variable, and the central bank can choose to set the rate of inflation or the nominal rate of interest, but not both.

Interest rates are correlated with inflation because the Fed historically raises interest rates when inflation rate is high.

This is an obviously true observation and easily borne out by looking at history.

Long term rates are distorted by QE right now. The market will price long term rates higher, when inflation is higher, sure.

Short term rates typically set a floor on long term rates, outside of rare yield curve inversions.

So not sure how your data relates. Short term rates set a floor on longer term rates, thus raising short term rates increases real rates on both fronts.

Long-term rates are not the same thing as rates in the long run. In the short run, monetary policy can create an imbalance and move the real rate of interest temporarily, but the real rate will adjust to its natural level as markets return to equilibrium, in the medium term. This is known as the Fisher hypothesis.

{kind=link}