You seem to be in agreement with me then. Higher nominal rates will also lead to lower inflation, thus pushing real rates even higher. So a hike acts on both the inflation side and nominal rate side to push real rates higher.

But speaking to the immediate circumstances, the fed primarily influences the short end of the rate curve. (Once QE is ended)

If the fed were to surprise hike interest rates this week, you can bet yields on the long end of the curve would come down.

Because the market would anticipate a hike in short term rates leading to end of inflation fears, and potentially triggering a deflationary event due to the surprise nature of it.

E.g. recall the times when the yield curve becomes inverted.

You can see over the past two weeks the yield curve has started inching towards an inversion. Actually the 20yr and 30yr inverted for the first time ever last week.

It's only speculation to say what this means, but to me seems a pretty obvious signal that the market expects the Fed to have to tighten faster than they're saying to curb inflation.

E.g. look at how quickly the 2yr has risen, while the 10yr has been in decline

Of course this inversion move is almost entirely due to how slow the Fed has moved. If they had moved faster, there would be less concern with a tightening. Now they may be late to the game if inflation pressures don't begin to ease soon.

We may actually be at full employment already, due to lifestyle changes leading to permanently lower labor force participation rate. In which case the Fed is years behind the curve on tightening. We'll know after a few more employment reports.

No, we are in disagreement. I agree with the view that the real rate is determined by the supply of savings and the demand for funds. According to this view, in the context of monetary policy, the real rate of interest is an exogenous variable, and the central bank can choose to set the rate of inflation or the nominal rate of interest, but not both.

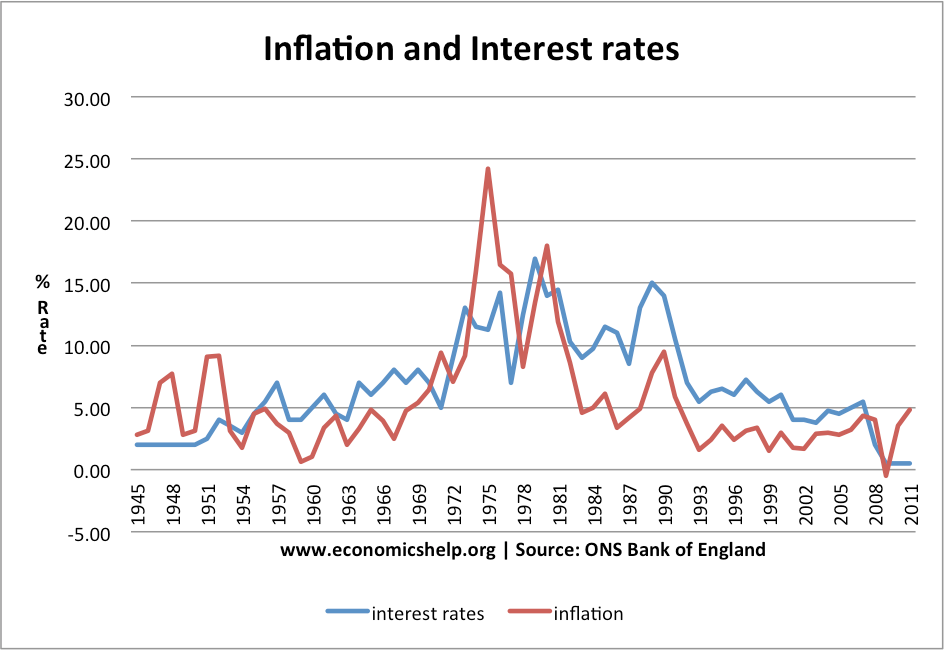

Interest rates are correlated with inflation because the Fed historically raises interest rates when inflation rate is high.

This is an obviously true observation and easily borne out by looking at history.

Long term rates are distorted by QE right now. The market will price long term rates higher, when inflation is higher, sure.

Short term rates typically set a floor on long term rates, outside of rare yield curve inversions.

So not sure how your data relates. Short term rates set a floor on longer term rates, thus raising short term rates increases real rates on both fronts.

Long-term rates are not the same thing as rates in the long run. In the short run, monetary policy can create an imbalance and move the real rate of interest temporarily, but the real rate will adjust to its natural level as markets return to equilibrium, in the medium term. This is known as the Fisher hypothesis.

{kind=link}

But speaking to the immediate circumstances, the fed primarily influences the short end of the rate curve. (Once QE is ended)

If the fed were to surprise hike interest rates this week, you can bet yields on the long end of the curve would come down.

Because the market would anticipate a hike in short term rates leading to end of inflation fears, and potentially triggering a deflationary event due to the surprise nature of it.

E.g. recall the times when the yield curve becomes inverted.

You can see over the past two weeks the yield curve has started inching towards an inversion. Actually the 20yr and 30yr inverted for the first time ever last week.

It's only speculation to say what this means, but to me seems a pretty obvious signal that the market expects the Fed to have to tighten faster than they're saying to curb inflation.

E.g. look at how quickly the 2yr has risen, while the 10yr has been in decline

Of course this inversion move is almost entirely due to how slow the Fed has moved. If they had moved faster, there would be less concern with a tightening. Now they may be late to the game if inflation pressures don't begin to ease soon.

We may actually be at full employment already, due to lifestyle changes leading to permanently lower labor force participation rate. In which case the Fed is years behind the curve on tightening. We'll know after a few more employment reports.